How to Tell Routing and Account Number on Check

A routing number is a nine-digit code used to identify a financial institution in the United States. Banks use routing numbers to direct the exchange of funds to and from one another. You can typically find the routing number on the bottom left corner of most personal checks.

- How to Find a Routing Number

- What's the Difference Between ABA and ACH Routing Numbers?

- What's the Difference Between ACH and Wire Transfers?

- What are SWIFT and IBAN codes?

How to Find a Routing Number

Routing numbers were originally created by the American Bankers Association (ABA) to streamline the circulation of paper checks on a massive scale. They are commonly referred to as ABA routing numbers or American Clearing House (ACH) routing numbers, and can be found on personal checks, bank websites or the ABA's online database. We link to different sources below.

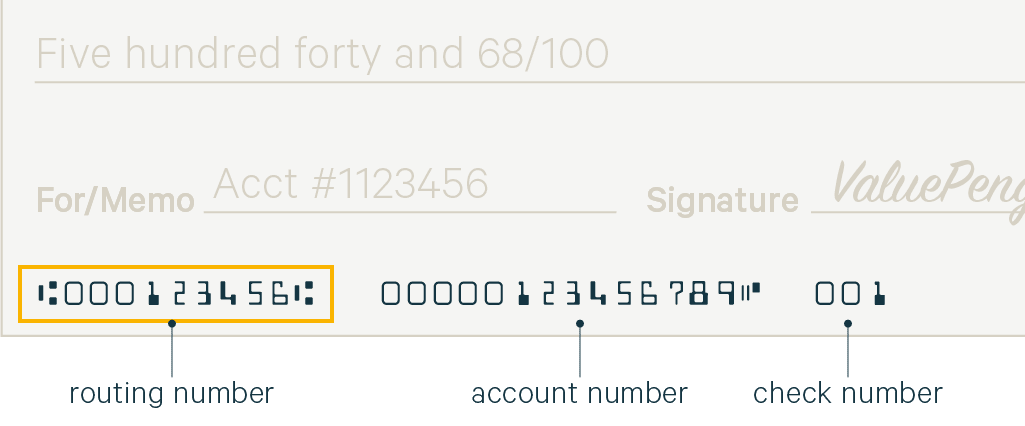

Where is the Routing Number on a Check?

The routing number and your personal account number can both be found on the bottom of the checks issued by your bank. Most banks provide at least one free checkbook for new customers.

Routing Number: The routing number consists of nine digits printed on the bottom-left corner of your check. The odd font used to print the number is known as magnetic ink character recognition (MICR) and is printed in electronic ink to allow banking institutions to easily process checks.

Account Number: The account number is located in the bottom center of your personal check, just to the right of your routing number. The account number is the unique identifier for your bank account.

Check Number: To help you keep a record of all payments, the bottom right corner of your personal check contains a unique check number.

When providing routing and account numbers, it's crucial to double-check your entries because errors can lead to failed transfers or send your money to the wrong account. If you catch an error, notify your bank so it can reverse the transaction. For more information, read our detailed guide to writing checks.

How to Find a Routing Number Without a Check

If you don't have a checkbook, you can still find your routing number by checking your bank's website or calling your local branch. The routing number varies by bank and region. Since one bank can have multiple routing numbers, be sure to confirm that your routing number corresponds to the specific bank where you opened your account.

We've included a list of some of the major national lending institutions with links to their respective routing numbers.

How to Find a Bank with a Routing Number (ABA Search)

If you wish to look up a bank by its routing number, you can search for it on the ABA's website. Additionally, you can also search for routing numbers through their website by inputting the bank's name and address.

It's possible to receive checks without a bank name. Technically speaking, the Federal Reserve system processes transactions as long as they receive the bank routing number and account number. This is why it's so important to protect your personal account number as carefully as you protect your social security number.

What's the Difference Between ABA and ACH Routing Numbers?

Technically speaking, ABA routing numbers apply to paper checks while ACH routing numbers apply to electronic transfers and withdrawals. Most major banks today use the same routing number for both. However, it's not uncommon to see separate ABA and ACH routing numbers for regional lending institutions.

ABA routing numbers are sometimes referred to as the "check routing number," and the ACH routing number as the "electronic routing number" or "number for electronic transfers." If only one number is cited, it's likely that the ABA and ACH routing numbers are the same, but it doesn't hurt to contact your bank to make sure.

What's the Difference Between ACH and Wire Transfers?

ACH transfers are automated electronic transfers between financial institutions which are conducted through a third-party clearinghouse. By contrast, wire transfers are direct electronic transfers between financial institutions.

Wire transfers are processed quicker than ACH transfers since they are not cleared through a third party. Wire transfers can be completed within hours or even minutes of when they're filed, while ACH transfers may take a few days. Wire transfers are also considered more secure because each bank must verify the transaction before it clears, while ACH transfers usually clear automatically.

We find that banks typically charge between $15 and $65 to send and receive wire transfers, whereas ACH transfers are generally free. Due to the added cost, wire transfers are best used for essential purchases involving large amounts, or transfers where the funds must arrive in a timely fashion. ACH transfers are sufficient for everyday transactions.

What are SWIFT and IBAN Codes?

Society for Worldwide Interbank Financial Telecommunication (SWIFT) is a code that identifies the bank in an international transaction, just as an ABA or ACH number identifies a bank in a U.S. domestic transaction.

International Bank Account Number (IBAN) identifies your personal account in an international transaction. It's usually the same as your regular account number with a few additional digits added in an internationally recognizable format. If you need to send funds internationally, ask the recipient for the IBAN number of their bank account.

SWIFT and IBAN were both developed to standardize an international identification system for financial institutions. While the United States uses the ABA system of transactions locally, American banks accept and transmit funds using the SWIFT system for multinational transactions.

How to Tell Routing and Account Number on Check

Source: https://www.valuepenguin.com/banking/what-is-a-routing-number

0 Response to "How to Tell Routing and Account Number on Check"

Post a Comment